The ECB has announced it will be hiking rates in July and September to counter record inflation.

Daniel Roland | Afp | Getty Images

U.S. political strategist James Carville famously said he would like to be reincarnated as the bond market because “you can intimidate everyone.” So when bond yields start signaling a problem, the whole market listens.

The escalatory rhetoric around the war in the Middle East has led to what Deutsche Bank is calling “the most hawkish central bank pricing of the year so far for both the [European Central Bank] and the Fed.”

Last week, sovereign bonds sold off across the board, with Europe as the epicenter. 10 year bunds hit their highest level since October 2023, while France’s 10 year OAT yield rose to highs not seen since the European debt crisis of 2011. U.K. gilts followed the same path, with the 10-year yield reaching its highest level in at least six months, driving markets to price in an 82% probability of a Bank of England rate hike this year. That’s right — a hike!

Across the Atlantic, predictions for the Federal Reserve’s ability to cut rates has dropped dramatically, with just 20 basis points of cuts priced in by the end of the year. That means — that for the first time — a 2026 rate cut from the Fed is now no longer fully priced in, according to Deutsche Bank.

Altaf Kassam from State Street Investment Management told CNBC that “central banks can look through temporary energy shocks, but persistent inflation risks will delay easing,” adding that in the event of an extreme shock, there could be a renewed tightening bias.

First up, the Fed

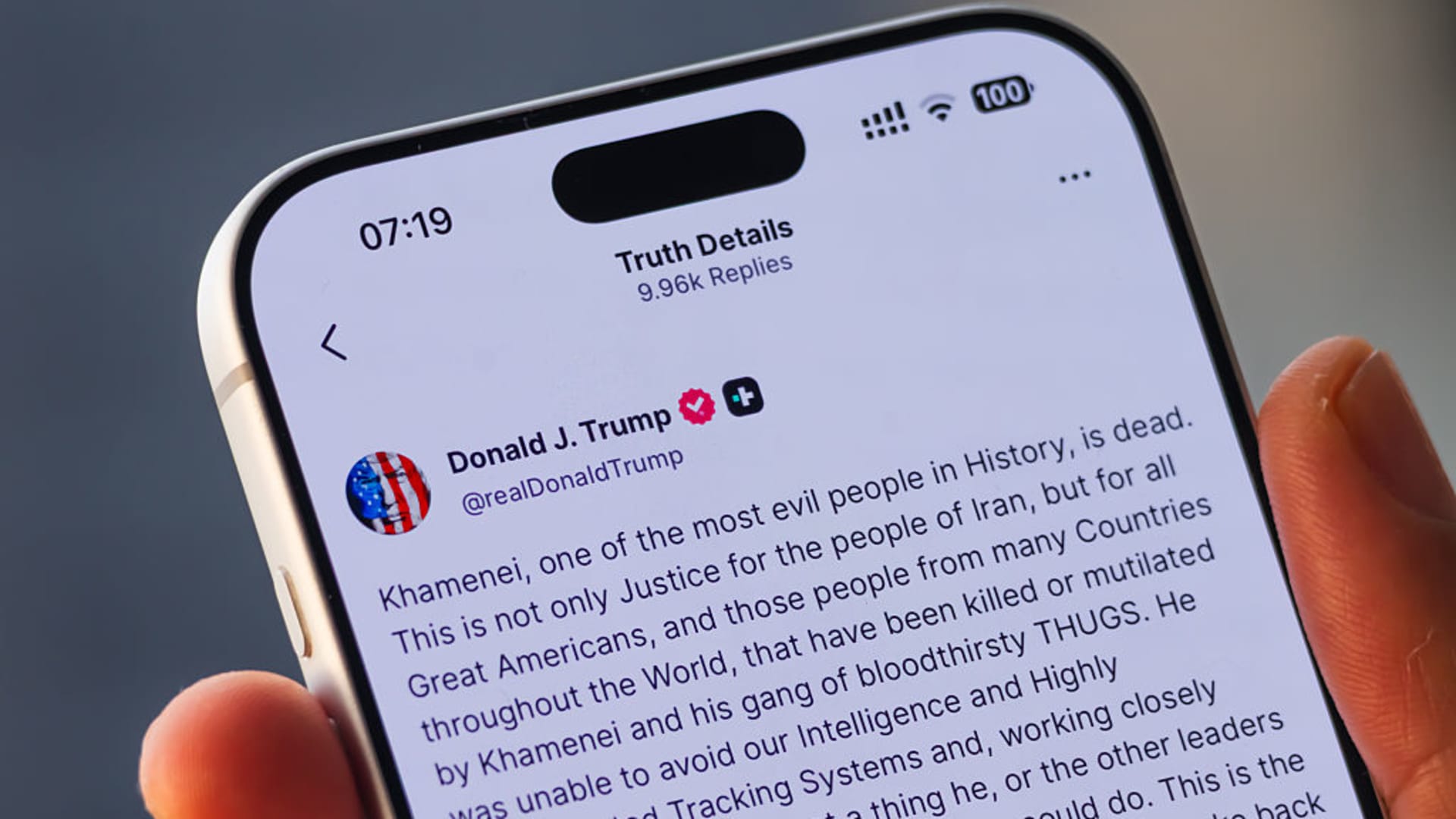

President Donald Trump has renewed his attacks on the Federal Reserve, taking to Truth Social to ask, “Where is the Federal Reserve Chairman, Jerome “Too Late” Powell, today? He should be dropping Interest Rates, IMMEDIATELY.”

However, in recent days traders have abandoned hope of easing from the Fed, with reducing odds of a cut this year. EY-Parthenon Chief Economist Gregory Daco said in a recent note that there is now an elevated chance that Powell “could continue leading the FOMC even after May”, due to the current market conditions. The Fed begins its two-day meeting on Tuesday.

A livestream shows Jerome Powell, chairman of the US Federal Reserve, speaking after a Federal Open Market Committee (FOMC) meeting on the floor of the New York Stock Exchange (NYSE) in New York, US, on Wednesday, Jan. 28, 2026.

Michael Nagle | Bloomberg | Getty Images

Wait and see for the ECB?

ECB President Christine Lagarde said the European economy was in a better position to absorb an inflation shock, telling France 2: “We will do all that is necessary to ensure inflation is under control.”

Analysts are less convinced, with BNP Paribas saying the uncertainty around Iran will “rattle the ECB’s ‘good place’ narrative.” The consensus expectation is for the central bank to hold rates on Thursday, however, in a recent interview with Bloomberg, Governing Council member Peter Kazimir suggested policymakers could opt for hike rates sooner than expected.

Keep it boring, BOE

The Bank of England is expected to keep interest rates on hold at 3.75% when it meets on Thursday. In a recent note, Oxford Economics outlined a worst-case scenario where oil rises to $140 a barrel, which could drive inflation much higher and send the U.K. economy into a mild recession.

A person shields themselves from the rain while walking near the Bank of England building on the day the Monetary Policy Committee lowered interest rates, in London, Britain, Dec.18, 2025.

Toby Melville | Reuters

Global Central Bank meetings this week

Monday: Reserve Bank of Australia Day 1

Tuesday: Reserve Bank of Australia Day 2, Federal Reserve FOMC Day 1

Wednesday: Federal Reserve FOMC Day 2, Bank of Canada

Thursday: Bank of England, European Central Bank, Swiss National Bank, Sweden’s Riksbank